July 2026

Is the housing slump creating buying opportunities?

June saw the downturn in Australia’s housing market further deepen, with Cotality’s national Home Value Index falling 0.4 percent in month-on-month terms, for the largest decline since December 2022.

The disparity in home price growth rates across the capital cities was once again apparent, highlighting the increasingly fragmented character of the Australian housing market.

The smaller capital cities still managed to eke out gains in home prices, with Darwin seeing a 1.4 percent increase and Perth a 0.7 percent rise. Brisbane home prices also remained buoyant, edging up 0.3 percent.

Both of Australia’s largest cities saw home prices slide, with Sydney posting a 1.2 percent decline and Melbourne falling 1.0%.

Source: Cotality

Tax changes and rate hikes

Rob Flux, founder of Property Developer Network, said recent changes to capital gains taxes alongside the Reserve Bank of Australia’s (RBA) continued hawkish stance were the key drivers of weakness in the Australian housing market.

“The combination of budget impacts and recent interest rate hikes has resulted in a softening of the markets in Sydney and Melbourne in particular.

“While the rest of the country is still in positive territory, growth has slowed significantly”

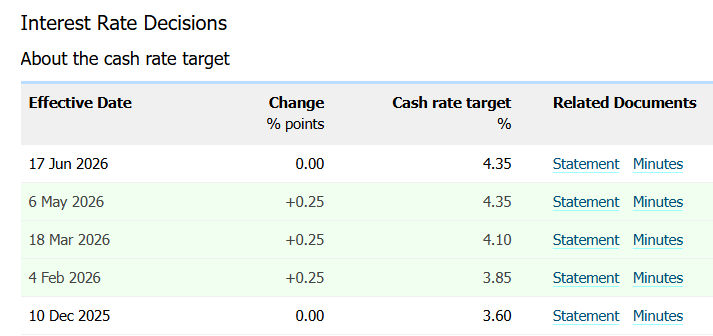

June marked the third RBA interest hike this year in response to inflationary pressure heightened by the conflict in the Strait of Hormuz. These three hikes have collectively lifted the RBA’s cash rate target from 3.6 percent to 4.35 percent, with the monetary authority signalling the possibility of further increases.

Source: RBA

The RBA also highlighted the adverse effect of the federal government’s landmark budget tax reforms on housing prices.

“Conditions in the established housing market had softened and housing credit growth looked set to slow in the period ahead,” the RBA said in its June statement.

Clearance rates slump

A further sign of weakness in the Australian property market can be found in its extremely low clearance rates, which fell below the 50 percent threshold nationwide through the second half of June, and for a third consecutive week at the start of July.

Clearance rates across Australia dropped to around 43 percent by the end of June, well below the decade average of roughly 65 percent.

David Ingram, CEO of CrowdProperty Australia, highlighted the data as a concerning sign for future housing price trends.

“The persistently low level of clearance rates bodes poorly for the market moving forward,” Ingram said.

“Potential buyers are holding off on entering the market, due to expectations of further declines in dwelling prices.”

Opportunities for developers

Despite the negative sentiment surrounding housing prices as a result of Australia’s macroeconomic policy environment, Rob Flux still sees reason for SME developers to be hopeful.

This is because the budget changes will favour demand for new build properties, as part of efforts to incentivise the development of new housing stock.

“There will be a huge number of buying opportunities coming into the market, with less competition, given investors are no longer looking at existing stock or second-hand properties,” Flux said.

“The next 12 months will see the emergence of a two-tiered market with a huge amount of demand for brand new stock.

“That means we’re now entering a season where property development is going to be more profitable than it has been for a long period of time.”

“While much uncertainty surrounds the changes to the capital gains tax, we still expect this to be a positive shift for the developer community over the long run,” Ingram said.

“The nature of these changes should translate into a rise in demand for the types of new housing products that smaller developers are best positioned to supply.”

CrowdProperty provides fast, simple and transparent property project finance for property professionals, learn more.

Opinions or views expressed represent the thoughts of individuals and not those of CrowdProperty or Quay.

June 2026

Australian home prices flatlined in May, as the Reserve Bank of Australia (RBA) extended its cycle of interest rate hikes in response to untamed inflation.

The Albanese government also introduced landmark tax changes that seek to improve home affordability by limiting the ability of investors to engage in negative gearing.

These changes, however, could create buying opportunities in the near-term while stepping up demand for new builds once they come into effect next year.

Australia home prices plateau

Nationwide home prices in Australia held stationary in May, with Cotality’s national Home Value Index coming in at 0.0%.

Australia’s two most popular cities accounted for much of the flatlining, with Sydney dwelling prices falling 0.9% in May and Melbourne’s housing market posting a 0.8% decline. Sydney is now 2.1% below its cyclical high in November of last year, while Melbourne is down 2.9%.

While other capitals continued to post gains, the impetus beneath housing prices is flagging. Perth and Darwin saw the strongest monthly growth in May with a 1.5% rise, while Brisbane and Hobart saw 0.9% increases and Adelaide rose 0.5%.

Tim Lawless, Cotality research director, said this diverging performance had been characteristic of Australia’s housing market since the pandemic.

“We are continuing to see multi-speed conditions across Australia’s housing sector, with Perth and Melbourne at opposite ends of the spectrum.”

“The past five years have seen these cities diverge sharply, with Perth values up a stunning 91.4% while Melbourne home values are only 3.3% higher since May 2021.”

Housing fundamentals remain unchanged

Key headwinds for Australia’s housing market at present include an environment of rising interest rates – following the RBA’s decision to lift the cash rate by 25 basis points to 4.35% in May.

Even more importantly, when it comes to structural trends on the Australian housing market was the latest budget, which introduced tax changes that will restrict negative gearing to new properties from July 2027.

The changes also replace Australia’s 50 per cent capital gains tax discount with a rate adjusted for inflation.

While the adjustments are intended to favour entrants to the housing market, Michael Yardney of Metropole Property Strategists argues that the budget fails to address the real cause of Australia’s housing affordability problem, which is a supply issue.

As a consequence, the underlying fundamentals of the housing market point to the persistence of upward pressure on dwelling values, as supply continues to fall short of demand.

Yardney points out that this shortfall in supply is the result of labour shortages and higher materials costs, as well as limited access to finance and land and approval delays.

The latest data from the Australian Bureau of Statistics (ABS) indicates that the total number of dwellings approved fell 3.4 per cent in April to 16,710, while private sector housing approvals fell 1.0 per cent.

The slide in housing approvals arrives despite the official launch of the National Housing Accord nearly two years ago, with the goal of remedying Australia’s home affordability crisis with the creation of one million new, well-located homes over a five-year period.

Kevin You, senior fellow at the Institute of Public Affairs (IPA), points out that the Accord has never reached its minimum monthly target, and housing approvals are now lower than they were in the middle of the pandemic.

David Ingram, CEO of CrowdProperty Australia, said this failure to build enough new builds on schedule favours long-term price gains, irrespective of tax changes.

David Ingram, CEO of CrowdProperty Australia, said the current focus on a potential correction misses the longer-term picture.

“Even a 10 per cent correction takes us back to a market we were already calling unaffordable just a few years ago,” said Ingram. “The structural imbalance between housing supply and demand has not changed. Australia has failed to approve and fund the build of enough homes to meet population growth for decades.”

Tax changes to create opportunities

Rob Flux from Property Developer Network expects the budget’s tax changes to create opportunities for developers and investors in both the short-term and long-term, despite the uncertainty created by the policy.

“For the next 12 months, investors will stay away from the market, which is going to create huge buying opportunities for anyone who is not currently in a deal,” Flux said.

“Once we get to July 2027 and the changes come into effect, I see a huge increase in demand from investors for brand new products that create additional dwellings, because those are the only things that will get the 50% capital gains tax and negative gearing.”

“First home buyers will also receive incentives for buying brand new stock, further increasing demand.”

CrowdProperty provides fast, simple and transparent property project finance for property professionals, learn more.

Opinions or views expressed represent the thoughts of individuals and not those of CrowdProperty or Quay.

May 2026

Growth in Australian housing values has eased considerably as inflation and the war in Iran prompt the Reserve Bank of Australia (RBA) to turn hawkish and resume rate hikes.

Opportunities are likely to be found at the cheaper end of the housing market, which is seeing far stronger price growth due to Australia’s scarcity of affordable, entry-level homes.

Sydney and Melbourne home prices slide

Growth in Cotality’s national home value index came in at 0.3 percent for April, its lowest point since January 2025.

Nationwide growth in Australian housing prices was held back by the poor performance of the Sydney and Melbourne property markets, where dwelling values slid 0.6 percent over the month.

While the other capital cities continue to see home prices rise, the pace of growth has fallen across the board. Perth came in first with a 2.1 percent rise, followed by Darwin with a 1.3 percent increase, and Brisbane with a 1.2 percent lift.

Tim Lawless, Cotality’s research director, said Australia’s easing property market is expected to come under even greater pressure in the near-term, with the RBA resuming a tightening stance in response to the resurgence of inflation driven by the war in Iran and oil price shocks.

“The housing market was losing momentum from late last year as affordability and serviceability constraints weighed on demand,” he said.

“Now we have the additional downside pressure of higher interest rates, sentiment has fallen off a cliff, and rising inflation is set to drive the cost of debt even higher.”

On 5 May, the RBA announced it would hike its cash rate target by 25 basis points to 4.35 percent, due to concerns over a pickup in inflation as fuel and commodity prices rise.

Negative gearing budget changes create market uncertainty

This year’s much-anticipated federal budget has proposed a major change to Australia’s tax regime that could significantly impact the nationwide housing market.

Treasurer Jim Chalmers announced plans to remove the 50 percent capital gains tax (CGT) discount introduced by Peter Costello in 1999, a policy widely seen as helping drive the rise of negative gearing among Australian property investors.

Critics say the policy reshaped investor behaviour by making property investment more tax-effective, increasing competition for lower-priced homes and making it harder for first-home buyers to enter the market.

If legislated, the changes are expected to take effect from July next year, with Treasury estimating the reforms could help an additional 75,000 Australians become owner-occupiers over the coming decade, following years of declining home ownership rates.

Opportunities lie with cheaper homes

Developers should keep a sharp eye on the increasingly varied performances of Australia’s many different property sub-markets, with cheaper housing expected to hold up better under the pressure of higher interest rates, particularly amid uncertainty surrounding the federal budget’s proposed changes to the CGT discount.

Michael Yardney, founder of Metropole Property Strategists, indicated the Australian property market has fragmented into a slew of highly varied micro-markets all moving in different directions.

These property sub-markets aren’t just spread across Australia’s many geographic regions, they often co-exist, with home prices in one area performing very differently to those in directly adjacent areas.

“The Australian property market isn’t just moving in different directions across cities,” Yardney writes. “It’s splitting within the same city, sometimes within the same suburb.”

Nerida Conisbee, chief economist at Ray White, uses the expression “K-Turn” to describe the stark divergence in the performance of Australia’s housing micro-markets.

Given worsening home affordability in the wake of sustained growth in dwelling values, premium Australian residential properties are struggling to achieve price gains.

Cheaper housing in the same areas continues to see strong price growth, as the very same affordability challenges heighten demand for down-market properties.

According to Conisbee, since 2023 the Sydney housing market has exemplified this divergence in home price performance.

Cheaper housing at the 25th percentile of the Sydney market has seen price gains twice as rapid as those of more expensive properties at the 75th percentile.

This means that even if interest rate hikes induce a downturn in the housing market, prices for cheaper properties could remain robust due to Australia’s worsening scarcity of affordable entry-level homes.

Yardney points out that over the past decade, national house sales under $750,000 have plunged, from around 248,000 in 2015 to just 153,000 in 2025.

As a consequence, developers and investors should pay close attention to opportunities at the cheaper end of the market, keeping in mind that these opportunities could be found within larger regional markets that are posting an overall sluggish performance.

While cheaper housing shows stronger price growth, Sydney’s development economics make this the hardest segment to deliver profitably. Building an apartment now costs $608,200 on average, up 90% since 2019, making entry-level product unviable at prices the market can absorb. Sydney developers have rationally focused on the downsizer and premium segment, where asset-rich baby boomers rightsizing into larger apartments can absorb delivery costs. The economics work; the sentiment fits.

Whether the 2026 budget changes this calculus remains to be seen. Limiting negative gearing to new builds and a new $2 billion Local Infrastructure Fund may improve feasibility at the margins, but construction cost barriers go unaddressed. Treasury’s own modelling suggests roughly 7,500 additional first-home purchases per year over the next decade is meaningful, but modest against the scale of Sydney’s undersupply. As CrowdProperty’s David Ingram puts it: “The 2026 budget takes some steps in the right direction — limiting negative gearing to new builds and committing $2 billion to local infrastructure are welcome signals. But none of this touches the core problem: it still costs more to build an apartment than most buyers can pay. Until we solve that equation, the supply we need won’t get built.” For developers, the smarter near-term play still points firmly toward the mid-to-upper market.

CrowdProperty provides fast, simple and transparent property project finance for property professionals, learn more.

Opinions or views expressed represent the thoughts of individuals and not those of CrowdProperty or Quay.